- Option Income Project

- Posts

- Powell Had His Pow Wow. The Markets Threw Their Teddy. Is the Crash Window Finally Opening? | SPX Market Briefing | 19 Mar 2026

Powell Had His Pow Wow. The Markets Threw Their Teddy. Is the Crash Window Finally Opening? | SPX Market Briefing | 19 Mar 2026

1 and Done Yesterday on Both Instruments – High Probabilities Don’t Care About the News

T2 Markets

March 19, 2026

Yesterday was a big news day. J-PowPow had his pow wow with the world and the markets didn’t like it one bit. Add into the mix the escalation of the Middle Eastern war – South Pars struck, the world’s largest natural gas reserve – and you get the markets throwing their teddy bear out the pram.

All 12 sectors closed red. Dow to its lowest since November. The worst rate decision day since December 2024.

Now the question on everyone’s lips: is the bear sell-off in the crash window finally going to happen? Honestly – I hope so. We need a corrective movement. Just a cheeky little 10%’er would do nicely.

Yesterday’s commentary was right before the bull move turned around – literally flipping from bullish to bearish in less than an hour. Then it just meandered further down all day. The FOMC nonsense fueled it and here we are.

Gold has especially been impacted – the most recent rising VWAP has been reclaimed. VIX is outside its channel and fear is back on the menu.

The 1 and done approach on both instruments yesterday was absolutely the right call. High probabilities don’t care about the news. The setup is the setup. Follow the money flow.

Powell Spoke. Markets Sold. Bears Hope. The Setup Is the Setup.

Market Briefing:

Thursday 19 Mar. Wednesday closed: Dow -1.63% to lowest since November / S&P -1.4% / Nasdaq -1.46% – worst rate-decision session since December 2024.

All 12 sectors red. FOMC held at 3.5-3.75% unanimously except one dissent.

Dot plot raised 2026 inflation forecast to 2.7%, one cut penciled, seven members see zero cuts. Powell: “very difficult.”

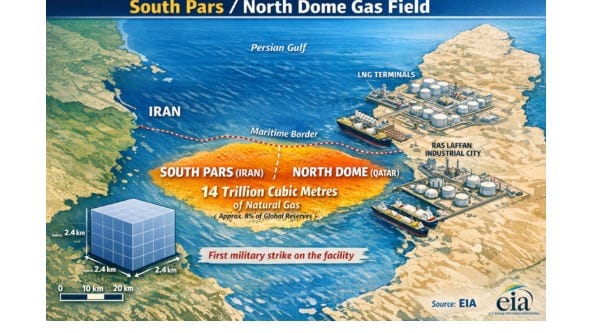

Israel and the US struck South Pars – world’s largest natural gas reserve shared with Qatar – Brent spiked to $109, up 80% since February 28.

Micron obliterated expectations after the bell: revenue $23.86B up 196% YoY, EPS $12.20 vs $8.79 expected.

Futures lower Thursday morning. VIX outside its channel. Fear back on the menu.

Market Snapshot

ES: 6,661.50 / FOMC hangover / worst rate day of 2026

YM: 46,452 / lowest since November / Dow -1.63% Wednesday

NQ: 24,562.50 / -1.46% Wednesday / Micron blowout after bell a rare bright spot

RTY: 2,483.4

GC: 4,701.0 / rising VWAP reclaimed / gold impacted by the overnight escalation

CL: 96.69 / Brent spiked $109 on South Pars strikes / up 80% since Feb 28

VIX: 25.80 / outside its channel / fear back on the menu

BTC/USD: 70,036 / coiling at $74K area / rate cut priced out / CLARITY Act Senate markup approaching

Tag ‘n Turn

Both instruments tagged bullish briefly on Wednesday and flipped back to bearish in under an hour. That is the read for this morning.

The PFZ flip was the signal to get more bearish on both. Being bearish since the beginning of February means there was no urgency to chase the Wednesday bullish tag – and that patience was validated inside the same session. Both signals now show Bearish Flipped with targets pending. A break below the marked lows on both instruments could see a nice pop and drop.

SPX Analysis

Bearish. Tagged bullish Wednesday, flipped back in under an hour. The triangle broke out, the SAR is in, and the bears are back in control.

The chart is annotated clearly – the triangle formation, the breakout, the SAR signal all visible. The TnT tagged Bullish briefly around the PFZ flip then reversed. The PFZ flip was the means to get more bearish, not a reason to go long. Given the bearish posture held since February, there was no rush to participate in the Wednesday bullish signal – it turned out to be correct to hold off.

The marked lows are the key level. A clean break below those could produce a meaningful pop and drop move.

Current Status: Bearish Below 6,666.52 (Flipped) / PFZ 6,680.04 / Target Pending / ATR 95.60 / watch the marked lows for pop and drop.

RUT Analysis

Uncle Russell is following the same playbook as SPX. Triangle, breakout, SAR, bearish flip. Same lows to watch.

RUT mirrored the SPX pattern exactly – tagged the Bullish TnT signal, couldn’t hold it, flipped back bearish. The triangle breakout is visible on the 30-minute chart. Same logic applies: a break below the marked lows sets up the pop and drop. Target pending on both instruments until price confirms.

Current Status: Bearish Below 2,493.27 (Flipped) / PFZ 2,499.33 / Target Pending / same lows as SPX to watch / pop and drop setup.

After Action Report – 18 Mar 2026 | Premium Popper | ORB20

1 and done on both. FOMC day. The right call.

SPX ran one trade. The 1st BO set up cleanly before the FOMC noise started. Covered at 66.7% ROC, $15 on the index. Done.

RUT ran one trade. Same approach – early 1st BO before the session got messy. 68.9% ROC, $5 on the index. Done.

Not aggressively hunting entries on FOMC day was wise. Prices meandered a lot before the official news happened and the exit finally appeared just after the formal announcement. The high probabilities don’t care about the news. The setup is the setup. Follow the money flow.

Current Status: 2 trades / 2 wins / 0 losses / 1 and done on each / FOMC day managed correctly

Rounding Off

South Pars changes the game. The joint Israel-US strike on South Pars – the world’s largest natural gas reserve, shared with Qatar – is a new order of escalation. Qatar condemned it. Iran named specific retaliatory targets: Saudi Aramco’s Samref refinery and UAE’s Al Hosn field. Brent at $109, up 80% since February 28. Every 10% rise in oil is 0.4% more inflation per the IMF. The Fed’s 2.7% revised forecast was set before South Pars. March CPI will reflect none of this.

The FOMC number that matters most. Seven members now project zero cuts in 2026. Not one. Not two. Seven voting for zero. The dot plot moved the 2026 inflation forecast to 2.7%. One cut is the median projection. The market had been pricing two. Powell’s “very difficult” framing was the most honest thing said in that press conference and the market treated it accordingly.

Micron is the outlier. Revenue $23.86B, up 196% year-on-year, up 75% sequentially. EPS $12.20 crushed the $8.79 consensus by 39%. Gross margin 74.9%. HBM4 in high-volume production for Nvidia Vera Rubin. In a session where all 12 sectors closed red, Micron after the bell was the only number that went the other way. AI chip demand is real regardless of what the macro does.

Current Status: South Pars struck / Brent $109 / seven FOMC members zero cuts / Micron +196% YoY / fear index 26 / VIX outside channel

Expert Insights

“Bull markets are born on pessimism, grown on skepticism, mature on optimism, and die on euphoria.”

– Sir John Templeton

The question this morning – is the crash window finally opening – is a pessimism question. The market has been in the pessimism-to-skepticism window for three weeks. Seven FOMC members projecting zero cuts. All 12 sectors red. Brent at $109. Consumer sentiment falling. University of Michigan respondents citing the Iran war directly.

Templeton’s point is that this is where bull markets are born, not where they die. That doesn’t mean the correction is over. A cheeky 10%’er from here would be the healthy flush that sets up the next move. The bears need to drive it home through the marked lows. The process stays the same regardless.

[Source: Sir John Templeton quote – widely attributed, public domain | FOMC statement – federalreserve.gov | Micron earnings – MU investor relations, public, 18 March 2026]

Beep-Beep.

1 – Seven FOMC members projecting zero 2026 cuts is a structural shift in Fed communication, not a data revision. The move from one consensus cut to seven zero-cut projections happened in a single meeting cycle. [Source: Federal Reserve Summary of Economic Projections, March 2026, federalreserve.gov]. This is not the Fed nudging the market – this is the Fed telling the market that the traditional rate-cut-as-rescue mechanism is no longer the assumed response to weakness. Markets have been buying dips partly on the assumption that the Fed would eventually ease. That assumption has seven official dissents against it now.

2 – The South Pars strike represents the first direct attack on a facility Qatar co-owns, which introduces a new diplomatic dimension to the conflict. Qatar hosts the largest US air base in the Middle East – Al Udeid. [Source: Reuters, AP geopolitical coverage, 18-19 March 2026, public]. A Qatari diplomatic rupture with the US over the strike would complicate logistics, base access, and regional coalition maintenance in ways that cannot be priced by an oil futures move alone. The Brent reaction to $109 prices the energy supply impact. It does not price the strategic base access risk.

3 – Micron’s 196% year-on-year revenue growth in the same session that all 12 sectors closed red is a specific signal about AI infrastructure spending. Hyperscalers are not cutting AI capex despite the macro headwinds. [Source: Micron Technology Q2 2026 earnings, micron.com, 18 March 2026]. HBM4 in high-volume production for Vera Rubin means the AI hardware stack is being built regardless of consumer sentiment, oil prices, or FOMC dots. The macro and the AI infrastructure cycle are running on different clocks.

In Other News…

The Federal Reserve held rates, raised its inflation forecast, penciled in one cut, and had seven members vote for zero cuts. Powell described the situation as “very difficult.” The market, which had been hoping for something closer to “manageable” or ideally “fine actually,” processed this in the traditional manner: down 1.4% with all 12 sectors red.

Consumer staples led the selloff. The sector specifically designed to hold up when everything else falls decided Wednesday was not the day to hold up. Healthcare and utilities, also in the “should be fine” category, followed consumer staples lower. The market’s defensive architecture had a structural failure on the same day the Fed confirmed stagflation risk. The timing was, to use Powell’s word, difficult.

South Pars was struck overnight. The world’s largest natural gas reserve. Qatar condemned it. Iran named specific targets for retaliation: Saudi Aramco’s Samref refinery and the UAE’s Al Hosn field. Brent hit $109. The IEA is presumably running out of superlatives for its reserve release announcements at this point.

Micron posted 196% revenue growth after the bell and EPS of $12.20 against an $8.79 expectation. In the context of an all-red session, geopolitical escalation, and the worst FOMC day of 2026, this number arrived like someone showing up to a funeral with a birthday cake. Technically correct. Slightly jarring. Appreciated nonetheless.

Fun Fact:

South Pars / North Dome is the world’s largest natural gas field, straddling the maritime border between Iran and Qatar. The Iranian side – South Pars – contains an estimated 14 trillion cubic meters of natural gas, representing approximately 8% of the world’s total proven reserves. Qatar’s North Dome side is the foundation of its LNG export industry, which makes Qatar one of the world’s top three LNG exporters.

[Source: U.S. Energy Information Administration – Qatar country analysis and Iran natural gas data – eia.gov | BP Statistical Review of World Energy, public]

The field has been in production since the late 1980s. Wednesday was the first time it was struck in a military operation. Context, as always, is everything.

Trade well,

T2 Markets

p.s. Want full access to the SPX Income System (includes 7+ mechanical income strategies)? Join our team now!

p.p.s. Want funding to DAY TRADE our options strategies? Discover how you can start trading with up to $250k of RISK FREE capital!

Reply