- Option Income Project

- Posts

- Hormuz Blocked. Banks Report. The Pop Lower Came And Went.

Hormuz Blocked. Banks Report. The Pop Lower Came And Went.

Brief premarket dip. Clean pop out of it. GEX showing massive exposure at 6,900. Eight days to April 22.

T2 Markets

April 14, 2026

The expected pop lower did happen — just briefly, in the premarket futures on Monday morning. And then price firmly broke up and out. Which is the continuation the 84% study, the BB pinch, and the bullish TnT were all pointing toward. The system does not care about the detour. It just cares about the destination.

Now. Banks.

Goldman delivered Monday. Profit up 19% to $5.63 billion. Revenue up 14% to $17.23 billion. Equities trading hit a record at $5.33 billion, up 27%. Investment banking fees up 48%. FICC fell 10% and missed estimates. GS shares dropped 2% on the beat — markets were pricing in more. Solomon warned: if the war drags, inflation trends become a headwind in Q2 and Q3. That is the template set.

Today the real test arrives. JPMorgan, Wells Fargo, Citigroup, and BlackRock all report before the open. PPI drops alongside them. One question dominates: how much is the Hormuz crisis costing corporate America? Dimon’s consumer credit metrics, delinquency trends, and the language around provision builds are the fulcrum of the day. If Dimon sounds calm, the market takes its cue. If Dimon sounds concerned, the market does the same.

Futures are retreating — S&P -0.59% to 6,814. VIX jumped 10.1% overnight to 21.17. The ten-year yield is at 4.317%. The blockade is active. Ceasefire expires April 22. Eight days.

But price broke up and out yesterday. The TnT is bullish on both instruments. And the GEX is showing massive exposure at 6,900 — that level will draw price like a magnet.

Pop Lower: Done. Price Broke Up. GEX Magnet At 6,900. Dimon Before The Bell. Eight Days To April 22.

Market Briefing:

Tuesday 14 Apr – bank earnings day.

Monday closed: S&P +1.02% to 6,886 / Dow +301 to 48,218 / Nasdaq +1.23% / recovery from Sunday’s -1.5% lows

Goldman: profit +19% / equities trading record +27% / IB fees +48% / FICC -10% miss / GS shares -2%

Solomon: prolonged Hormuz becomes Q2-Q3 inflation headwind

Pop lower happened briefly in premarket / price broke firmly up and out / continuation confirmed

Tuesday premarket: S&P futures -0.59% to 6,814 / Nasdaq -0.70% / Russell -0.98%

VIX +10.1% to 21.17 / 10-year yield 4.317% / stagflation arithmetic building

Today’s data: JPMorgan / Wells Fargo / Citigroup / BlackRock all before the open / PPI alongside

Dimon consumer credit metrics / delinquency trends / provision builds: the session fulcrum

Seven FOMC members project zero cuts 2026 / Fed median: one cut / Powell exits May 2026

Blockade active / ceasefire expires April 22 / eight days

Tuesday read: TnT bullish both instruments / GEX massive at 6,900 / flip point 6,667 / let the magnet work

Market Snapshot

ES: 6,935.00 / +7.50 (+0.11%) / broke up and out / holding the move

YM: 48,462 / +13 (+0.03%) / Dow resilient into bank earnings

NQ: 25,638.00 / +52.50 (+0.21%) / Nasdaq recovering

RTY: 2,693.70 / +7.80 (+0.29%) / Uncle Russell back up

GC: 4,799.90 / +33.30 (+0.70%) / near record / stagflation bid

CL: 97.11 / -0.90 (-0.92%) / blockade active / slightly off overnight

VIX: 18.30 / -0.81 (-4.24%) / through 22 / falling not rising / positive

BTC: 74,629.23 / +0.09% / recovered to $73,400 Monday / range playing out

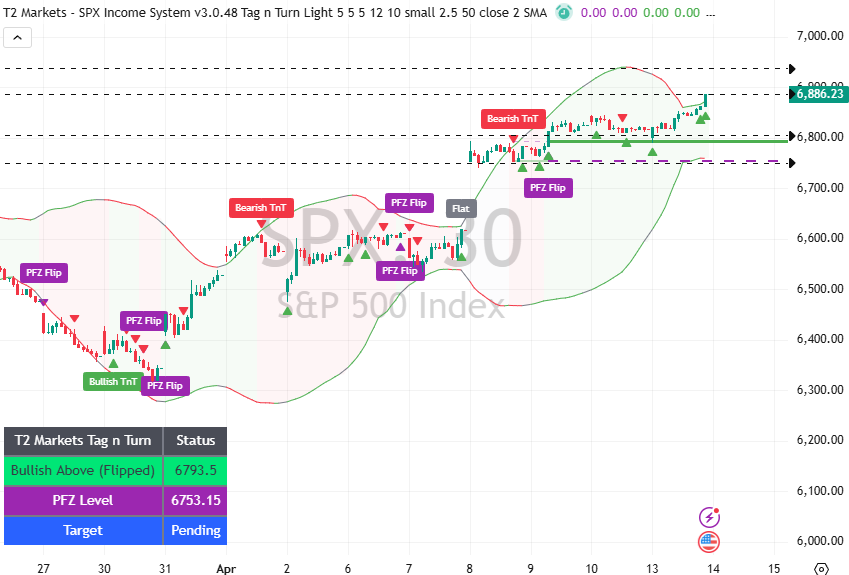

Tag ‘n Turn

Both instruments bullish. Price broke firmly up and out after the brief premarket pop lower. The continuation thesis is confirmed. GEX has massive exposure at 6,900 – the magnet is set.

Monday’s session delivered exactly what the research suggested was the most likely sequence: a brief pullback — the premarket dip — followed by a clean break upward through the range that had been building since the ceasefire bounce. Both TnT signals are bullish. The GEX picture makes 6,900 the logical target for today’s session given the concentration of gamma at that strike. The flip point at 6,667 is well below current price — 219 points of positive gamma cushion. The environment remains constructive. Let the magnet work.

SPX Analysis

Bullish above 6,793. Price broke up and out after the brief premarket pop lower. MACD-v building positive momentum again. 6,900 is the GEX magnet. Target pending the move establishing.

The chart is clean. The range that had been consolidating since the ceasefire bounce resolved upward on Monday — exactly as the 84% continuation study and the bullish TnT were pointing toward. The MACD-v on the 30-minute has turned up again after the reset. The BB has opened up following the pinch release. Price is above 6,800 and the GEX exposure at 6,900 provides the mechanical pull for the session. The brief premarket dip on Monday was the 2 April equivalent that the research anticipated — quick, shallow, then done.

Current Status: Bullish Above (Flipped) 6,793 / PFZ 6,753 / Target Pending

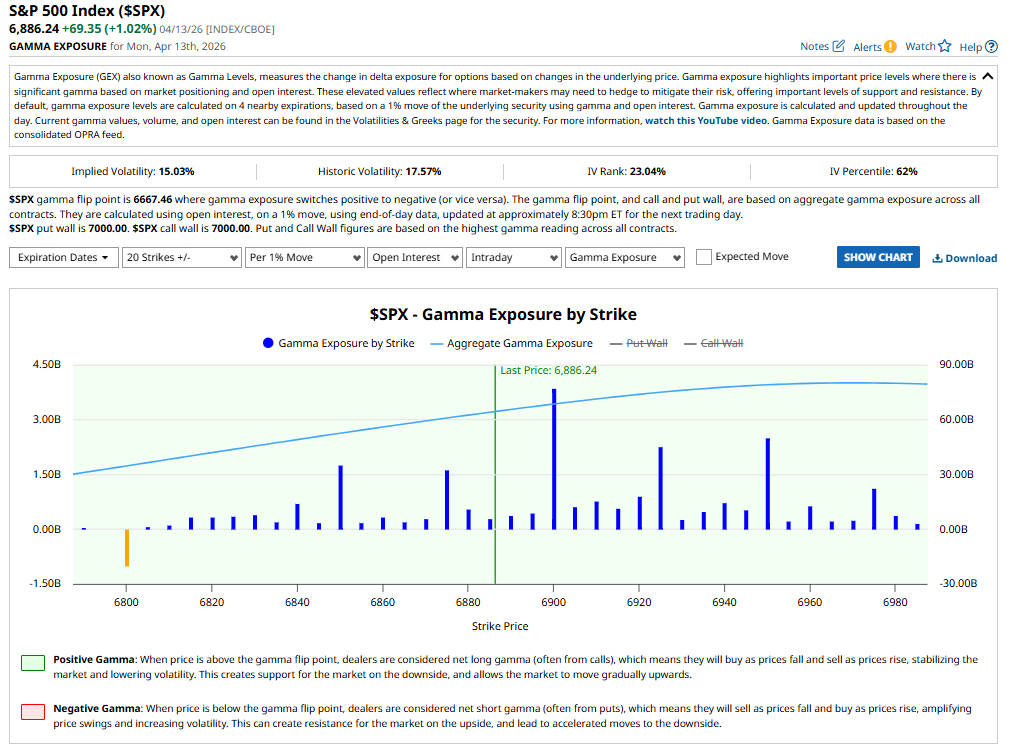

Gamma Exposure

Strongly positive. Flip point 6,667. Massive gamma exposure at 6,900. Both walls at 7,000. IV 15.03% well below HV 17.57%. IV Percentile 62%. Mechanical pull toward 6,900 is the read.

The aggregate GEX is at its strongest reading of the conflict. The concentration of gamma at the 6,900 strike is notable — a 3.5B+ spike at that level is the kind of gravitational pull that draws price during low-volatility sessions. With IV at 15.03% against historic vol of 17.57%, the market is pricing calm — dealers are stabilizing and the mechanical environment supports a steady grind toward 6,900. IV Percentile at 62% continues its compression from 96% six weeks ago. Put and call walls converged at 7,000. The flip point at 6,667 is 219 points below current price. The 6,900 magnet is the operative level for today.

Current Status: Strongly positive / flip point 6,667 / massive gamma at 6,900 / put wall 7,000 / call wall 7,000 / IV 15.03% below HV / IV Percentile 62%

RUT Analysis

Uncle Russell bullish above 6,793. Same clean break up and out. MACD-v resetting bullish. Same read as SPX — the magnet is working on both.

RUT mirrors the SPX picture — the brief premarket dip on Monday gave way to a clean break higher as the session established. The MACD-v has turned bullish again on the 30-minute chart. Both instruments are aligned, both broke out of their respective ranges, both are pointing toward the GEX magnets above. The bullish read is intact.

Current Status: Bullish Above (Flipped) 6,793 / PFZ 6,753 / Target Pending

Post Trade DeBriefing – 13 Apr 2026

SPX Lazy Popper: Data issues meant the ORB ranges had to be calculated manually. Two lines drawn. A few things counted. The horror. It worked.

Trade 1: Lazy Day Trade. 100% ROC from a $40 move. At 1r.

1 trade / 1 win / 0 losses.

SPX Premium Popper: Same session, same data workaround, same result.

Trade 1: 1st BO. 66.7% ROC from a $12 move. At 1r.

1 trade / 1 win / 0 losses.

2 trades total / 2 wins / 0 losses. The system does not care about data tool issues. It just needs two lines and a count. Noted for future reference.

Rounding Off

Dimon Today JPMorgan reports before the bell. The street estimates $5.38-5.50 EPS, up 7% year-on-year. The number matters less than the commentary. Dimon’s consumer credit metrics — delinquency trends, provision builds, CRE exposure under the oil shock — are the session’s fulcrum. Goldman set the template Monday: records on equities and IB, miss on FICC, warning on Q2-Q3. If Dimon echoes the warning on inflation headwinds, the market adjusts the second half of the year. If Dimon sounds comfortable, the rally has its confirmation.

Goldman’s Warning David Solomon’s Q2-Q3 inflation headwind comment is worth sitting with. It is not a disaster call — Goldman had a record quarter. But the framing acknowledges that the ceasefire-to-blockade sequence means the war cost has not yet fully shown up in corporate financials. Q1 was compiled before the blockade. Q2 will not have that luxury.

The Pop Lower: Filed Brief. Premarket. Done. Price broke firmly upward. The research called it — same configuration as 2 April, pop lower before the next bull leg. The pop lower arrived and left in approximately one premarket session. The bull leg followed immediately. The 84% continuation study continues to be 84%.

April 22 The ceasefire expires in eight days. Pakistan is attempting to restart talks. The blockade is active. These two facts are in tension and neither has resolved. The market is choosing to focus on the bank earnings today and deal with April 22 when it arrives.

Current Status: Bullish / GEX magnet 6,900 / Dimon before the bell / PPI alongside / April 22 eight days / blockade active / pop lower done

Expert Insights

“The four most expensive words in the English language are: this time it’s different.”

– Sir John Templeton, widely attributed across interviews and financial publications, public

Applied to Monday’s session specifically: every version of the morning’s news suggested the rally should not have worked — blockade active, Goldman below estimates on FICC, VIX spiking, futures down at the open.

And yet the brief pop lower was brief, the break higher was clean, and the TnT delivered exactly what the research said it would. The 84% is 84% regardless of the macro backdrop. The process does not need the environment to cooperate. It needs the signal to confirm. The signal confirmed. This time was not different.

[Source: Sir John Templeton — widely attributed across investor interviews, Forbes, and Fortune, various dates — public domain]

1 – Goldman’s FICC miss of approximately $400 million against a record equities quarter creates a specific diagnostic about where the war premium is being priced. FICC — fixed income, currencies, and commodities — underperformed in a quarter where commodities were the dominant global story. [Source: Goldman Sachs Q1 2026 earnings release, public | Analyst consensus data, public]. The underperformance is counterintuitive until the mechanism is examined: commodity volatility was extreme but directional, meaning clients reduced rather than increased hedging activity once the direction was clear. Record equities trading reflects client repositioning. FICC miss reflects clients who had already repositioned and were not adding incremental trades. Dimon’s FICC commentary today will either confirm or contradict this interpretation.

2 – PPI data releasing simultaneously with JPMorgan earnings creates a specific signal sequencing problem for the market. PPI measures upstream producer inflation — the prices businesses pay before passing costs to consumers. [Source: Bureau of Labor Statistics PPI methodology, bls.gov, public]. In a Hormuz blockade environment, energy-driven PPI spikes feed directly into PCE with a one to two month lag — which means the PCE that the Fed uses for rate decisions in late April and June will be elevated by today’s PPI reading. If PPI surprises to the upside alongside a cautious Dimon commentary, the market is simultaneously processing a hawkish inflation signal and a cautious corporate credit signal. Both point toward fewer cuts. The sequencing of those two data points in one morning session is the day’s primary risk.

3 – The April 22 ceasefire expiry is eight days away and the blockade has been in effect for four days. The asymmetry between the two timelines creates a specific negotiating dynamic: Iran is operating under blockade conditions during what remains technically a ceasefire period. [Source: Pakistan Foreign Ministry statement, public | US Central Command blockade announcement, public]. If the ceasefire expires without a new framework, the conflict returns to pre-ceasefire rules of engagement while the blockade remains in place. That combination — no ceasefire, active blockade — is the highest-escalation scenario of the conflict so far. Eight days. The banks answer today. The calendar answers on the 22nd.

In Other News…

Goldman reported Monday. Profit up 19%. Record equities quarter. FICC missed. Shares fell 2% on the beat. Solomon warned about Q2-Q3 if the war drags.

Monday’s session closed up 1.02% anyway. Price broke firmly upward after a brief premarket dip. The dip lasted approximately one premarket session. Then it was done.

Today: JPMorgan, Wells Fargo, Citigroup, and BlackRock all report before the open. PPI arrives alongside them. Dimon’s consumer credit commentary is the most watched signal. The question the whole earnings season is trying to answer: how much is the Hormuz crisis costing corporate America?

The blockade is active. The ceasefire expires in eight days. Futures are down 0.59% this morning. VIX jumped overnight. And the GEX has a 3.5 billion spike at 6,900 that draws price the way magnets draw price.

The system does not care about the detour. It cares about the destination. Yesterday’s data issues meant two lines were drawn manually and a few things were counted. The poppers popped regardless. This is the correct summary of what happened.

Fun Fact:

Jamie Dimon has led JPMorgan Chase since 2005, making him the longest-serving CEO of any major US bank and one of the longest-tenured leaders of any Fortune 500 company. He is known in financial circles for his annual shareholder letter — a document that functions as an informal State of the Union for the US economy and is read closely by policymakers, investors, and central bankers worldwide.

Dimon survived the 2008 financial crisis largely intact, was one of the first major bank CEOs to warn publicly about the risks of sustained inflation in 2021, and has consistently been among the most candid voices on geopolitical risk in his sector. When Dimon speaks about credit quality under an oil shock, the market listens — not because he is always right, but because he has more data than almost anyone else in the room.

[Source: JPMorgan Chase investor relations — annual shareholder letters, jpmorganchase.com, public |

Forbes and Bloomberg Dimon profile, various dates, public]

Trade well,

T2 Markets

p.s. Want full access to the SPX Income System (includes 7+ mechanical income strategies)? Join our team now!

p.p.s. Want funding to DAY TRADE our options strategies? Discover how you can start trading with up to $250k of RISK FREE capital!

Reply